There is a real change in market behavior when the maker fee is below the taker fee. This is because markets usually have a constraint, that in the order-book, the bids should be below the asks. So at some point a maker can not increase its buy-price or lower its sell-price.

This will result in a slightly less efficient market, because some transactions are not possible even when there is a maker and a taker available who are both willing to do the trade.

I think this lower efficiency works in favor of the makers, because the takers are usually more time constrained and are more willing to take a less favorable price.

You are right, I didn’t think about it that way. You can of course sell ether without being a market maker. I was thinking about the case where you put up a big sum of ether on the supply side. Of course, it may be better to use OTC services if that is the case.

As a whole, users are incentivized to engage in mechanisms that benefit either the exchange or siding to either becoming a maker, taker.

Reduce one area, we see a shift towards the other. However, entirely there is a set of people who find minimal maker, taker percentages less meaningful to their overall state.

The main reason why (as I personally understand it) exchanges arrange different maker-taker fees is purely to bring in different market participants to provide (or take, dependent on specific need) liquidity / activity to that particular exchange. Say if I maintain an exchange and I desperately want to have participants to provide the necessary liquidity, I will arrange to have 0% maker fee so that participants are more incentivized to post limit orders that will help to make my order book thick, and that will further attract more participants to trade at my exchange. Participants that are desperate enough for liquidity that they will trade at market order will care less about the 0.6% I would impose on them being takers because if they were to trade elsewhere that have much less liquidity, they would incur far higher costs like wider spread and slippage.

Not behavioral. Not cosmetic. Purely economic dependent on the need of the exchange.

For further study, please refer to topics on market microstructure.

My argument in the initial post showed that from a purely economic standpoint, you can prove that going from (0.3%, 0.3%) to (0%, 0.6%) should in equilibrium cause the nominal spread to shrink by 0.3%, so the real spread (ie. amount you can buy for including fees minus amount you can sell for including fees) is unchanged.

You can’t say that “participants are desperate for liquidity and so they are price insensitive”, because if that was true, the exchange would have already increased the fee from, say, (0.3%, 0.3%) to (0.3%, 0.6%) or even (0.6%, 0.6%).

I believe there is always inefficiencies that will remain persistent for a long time. And that includes the spread regardless of whether it will shrink by 0.3% or remain wide. At most, what an efficient participant can do is to exploit the inefficiencies but still that does not guarantee the inefficiencies will certainly fade away. In a market where everyone has equal footing, aggregate inefficiencies make it more efficient as a whole, but not perfectly so. In a market whereby we see 100% perfect efficiency always have participants that have unfair privileges. Because maintaining perfect efficiency incur costs that only a participant with unfair privileges can afford to maintain. The world of HFT (high-frequency trading) is a good example.

A desperate participant will certainly be price insensitive, no matter what logic says. This is because all trading is forward-looking, i.e. I expect the price will appreciate by 5%, everyone expects the same, the current price is at 1% premium, if I do not buy now but instead wait for it to fall by 1% before I do so, then I will forgo 4% return potential to other more aggressive participants that do not care to buy at premium. And thus, I will take the action to buy at 1% premium even though logic says it is inefficient as of now.

Indeed, if all participants are very desperate for liquidity and the exchange is the one and only dominant player around, then yes, it is very likely fee may be increased to (0.6%, 0.6%) or even (1.2%, 1.2%). But as there is stiff competition around, then such fee may not increase despite desperate participants. If human decision-making can be as efficient as computer logic, then the world may probably have no need for economics as nobody can be gamed.

If the maker-taker fee is purely cosmetic and not economic, then what do you think a newly-opened exchange should do to attract participants? How should the fee be set to attract both market makers and liquidity takers? The industry is so competitive that some exchanges are even offering rebates to market makers. Ultimately, the point of having differing fee structure is to attract participants to generate liquidity and activity to the exchange. How the fee is being structured, or sliced and diced between the different participants depends on the need of the exchange. I cannot think of any cosmetic reason other than economic ones.

How should the fee be set to attract both market makers and liquidity takers?

Honestly, if everyone else is doing maker-taker fees and that’s what attracts people for behavioral reasons, then go ahead and do that; it’s not like there’s any economic harm in doing it one way over another. But in general, I don’t think there’s anything you can do to incentivize a lower net spread into existence unless you are willing to pay for it, whether in lost revenues from lower total fees or from explicit subsidies.

That is why some exchanges are offering rebates, as you correctly pointed out by saying “unless you are willing to pay for it, whether in lost revenues from lower total fees or from explicit subsidies.” Exchanges that do not play the game in a fair manner try to minimize such cost of running the business by engaging in all sorts of nefarious activities, including front-running the participants and trading between their own accounts to give the illusion of liquidity. The behavioral reason is purely an economic one. Ultimately, it is all about making a profit.

I would submit a limit order of $1000 even when I mean to buy at $1003 if and only if I expect the market to go sideway within the duration of my order while it lasts. As the market is forward-looking and if I anticipate it will move up, I would not submit limit order of $1000. Probably I would do so at $1005 if market activity is very high. At the same time, I would also expect the limit sell order to be much higher than 0.3% spread as participants engage in FOMO, thus the “inefficiency.”

Yes, in a market whereby every participant has fixed supply of stuff to buy and sell that they cannot inflate or deflate at will, both costs and benefits of switching from one model to the other will be zero to all parties. Here, we are talking about taking the average. In reality, some will make lots of money while many others will lose lots of money.

An exchange does not have any interest in determining which participant will make lots of money and which other will lose lots of money. It cares only to structure the right maker-taker fees in accordance to its needs in order to attract all sorts of participants, winners and losers alike, to join the exchange and provide liquidity and activity so that it will earn fees from everyone. If it cannot do so at first through honest means, it will do so through nefarious means, including front-running, internalizing orders, sub-pennying, etc.

After going through the SEC memo on maker-taker fees very briefly, assuming I understand it correctly, the SEC is trying to review the current maker-taker fee structure for a possible revamp in order to create a fairer market for all participants and increase the liquidity.

If so, then I believe the increasing illiquidity has nothing to do with any form of maker-taker fee. Rather, it has to do with rampant HFT, sub-pennying, decimalization of share prices, etc that while it caused the spread to artificially narrow, it also took the market-making potential away from traditional market-makers and relentlessly exploit market participants through front-running. As a result of trying to make the market more efficient, exchanges engaged in unfair means that end up making it far more inefficient than ever. As result, liquidity declined over the years substantially.

You can find various books on HFT on how it gamed the market and sucks liquidity out of it. Revamping the maker-taker fee structure will not restore liquidity if all the market manipulations such as front-running and sub-pennying are not resolved. If I know I would lose in a highly manipulated market whereby the structure is generally fake, I would not trade in such market even if there is 0% fee.

For exchanges to fantasize it can get all the real liquidity it desires while allowing rampant manipulations to persist is foolish. No restructuring of the maker-taker fee will solve the problem.

Exchanges can restore liquidity by getting rid of HFT front-running, getting rid of sub-pennying, and centralizing the order books (instead of having lots of exchanges that end up fragmentalizing the liquidity) and let real liquidity to grow organically. Whatever the maker-taker fee structure can stay the same.

I realized that this does not steal any more liquidity after two exchanges reach an equilibrium, thus it should be entirely behavioral if it affected liquidity in real world exchanges - let me think twice before wasting valuable time of others…next time.

I have some more thoughts though - if we pay a rebate to market makers by taking it from takers (e.g. -0.3% maker fee and 0.9% taker fee), and the rebate happens to be greater than the average spread (i.e. the average spread < 0.6%), two exchanges never reach an equilibrium, right? Makers should be supplying liquidity on the ‘rebate’ exchange as long as takers consume the orders. This can be argued as behavioral but it reduces uncertainty on the maker’s side - they can confirm that desperate takers (willing to lose some additional 0~0.3%) exist on that exchange (which remains relatively stable over time), and serve them by sucking liquidity from other exchanges. It can enter a positive feedback loop - more immediate liquidity attracts more desperate takers (or I would say normal users), and more market makers enter this business for profit, moving liquidity in one direction. Does this make sense?

The question is about whether a per unit tax or subsidy to one side of a market is fully offset by a change in the price charged to the other side.

Under complete ‘pass through,’ subsidies are fully offset by price reductions and thus subsidies become completely inconsequential. Complete pass through could easily arise in a model, but is much less likely in real life.

Under incomplete ‘pass through,’ the side receiving the subsidy captures some value. The subsidy then encourages entry into the subsidized activity.

You will fail to get complete pass through if any of the following conditions hold:

There are ‘transaction costs’ that impede adjustment of prices.

Participants on at least one side of the market pay a fixed cost as well as a cost per unit.

The side receiving a subsidy is not perfectly competitive.

I would say that (1), (2), and (3) are all important reasons for incomplete pass through on exchanges.

For example:

(1) Many exchanges have minimum tick sizes. This limits makers ability to undercut one another. Once you have a minimum tick size, transaction costs make complete pass through impossible.

(2) Some orders originate from brokers. There is fixed fee component to retail brokerage fees.

(3) The business of market making is highly competitive as a whole. However, market making in at a specific asset/time/place can be much less so. For example, you would likely see greater pass through for highly liquid tokens where many market makers are active simultaneously. For a highly illiquid token, however, there may be only one or two market makers active at a time. In this case, more of the subsidy would be retained by the market makers, the narrowing of the bid ask spread via passthrough is smaller, the increase in the depth of liquidity available as a result of the subsidy is larger.

(Note: (3) implies that the subsidy primarily encourages entry into illiquid trading pairs. Interestingly, after entry, the incumbent market maker will capture less of the subsidy and there will be more pass through. Their is potentially a phenomenon where subsidies work to bootstrap new markets, but you move towards full pass through as the market matures. This is a nice feature because you usually want to selectively subsidize entrepreneurial activity. You do not want the subsidy to be captured by a market that could function effectively without it.)

The concluding section of the following paper has a really awesome and math free discussion of pass through:

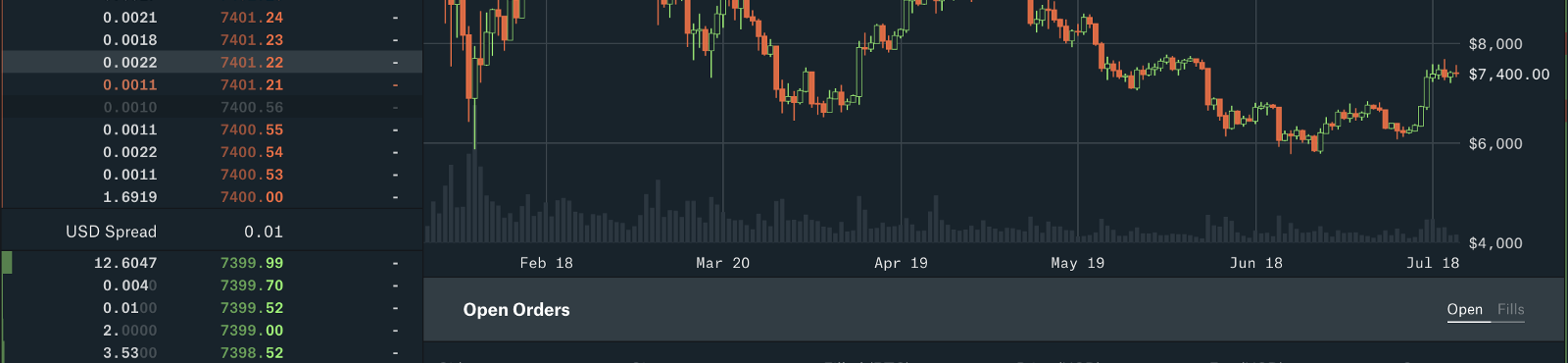

This is directly observable in the behavior of exchanges with reasonably sophisticated market participant access and high relative taker costs. For example on GDAX:

Note that the spread is a single cent ($0.01), the minimum tick size. This is a relative bid-ask spread of 0.00013% or .013 BPS at that price level. Credit Suisse publishes yearly data on US equities relative spread trends:

Implies about a 200x multiple on average relative spread US equities vs GDAX. Considering that Bitcoin is a far more volatile asset than the average US equity (and the spread makers are willing to offer should be directly related to volatility) one could reasonably conclude that the phenomenon is the result of sophisticated actors, who would otherwise be takers, meeting at a 1c spread, waiting for either (1) an unsophisticated retail trader to naively take the order, or (2) a more informed sophisticated actor to take it once their predicted change is > the cost of taking it (in this case, the cost being 0.1%-0.3% of notional trade value that GDAX charges).

Interestingly, traditional equities and commodities markets charge flat fees (e.g. 0.25c/share) instead of “% of notional trade value” fees that are common in crypto. It basically means that actor (2) in the above must always be able to reliably predict change in BTC value >= 0.1-0.3% in order to make any liquidity taking order worth it. As the cost of a taker order goes to zero the amount of time expected for that much volatility also goes to zero so you would see less time spent sitting at a 1c spread.

You can check the spread yourself, right now and every other time I’ve looked it’s at or quickly approaching 1c (screenshot above isn’t cherrypicked). I suspect that if the tick size were to be arbitrarily more granular it wouldn’t matter and the spread would continue to approach it (e.g. we’d still be sitting at a $1e-5 spread if that level of tick resolution was offered).

I think this line of reasoning fails to take into account the other argument that I added to the end of my post: that a maker/taker fee model is isomorphic to a change in the user interface. I agree that fixed tick sizes are a good reason why maker/taker models would not be no-ops, but (2) and (3) do not change the basic reality of my argument, which does not make any assumptions about cost structure or competitiveness.

In the maker-taker model, the makers implicitly participate in a price fixing agreement, they agree not to put in a price such that the bid would be equal or larger than the ask. This is because the exchange would otherwise interpret that as a take order with higher fees.

In the interface analogy, this will result in the interface not accepting certain orders that will result in zero or negative spreads.

Suppose a buyer wants to buy at x after fees, and a seller wants to sell x-0.1% after fees.

In a 0.3%-0.3% market this will result in a bid of x-0.3%, and ask of x+0.2%, a 0.5% spread.

In a 0%-0.6% maker-taker market this will result in a bid of x%, and ask of x-0.1%, a -0.1 spread. Negative spreads are not allowed, so given the buy order, the seller is only allowed to sell at higher than x or take a price of x-0.6%.

This price-fixing is profitable for the makers, because they are getting a better price than they would otherwise get.

Participants on at least one side of the market pay a fixed cost as well as a cost per unit.

Many retail investors purchase securities from brokers who charges a fixed fee per trade. The broker is legally obligated to purchase the security at whichever exchange offers the best asking price. The legal requirement does not incorporate taker fees charged by the exchange when computing the best asking price. As a result, a disproportionate amount of retail order flow is routed to exchanges that compensate market makers via taker fee rebates rather than through the bid-ask spread.

I think if one searches carefully, it would be possible to identify other types of fixed costs that prevent full pass through. For example, maker rebates are often tiered, so that a maker receives a larger and larger % rebate as he drives more traffic to the exchange. In effect, this is similar to charging makers a tiered membership fee (a type of fixed cost).

Models cannot easily account for all these types of frictions and thus have a tendency to exaggerate pass through.

The side receiving a subsidy is not perfectly competitive.

This is complicated. I believe that this will boil down to some type of implicit collusion as suggested by the previous poster. I agree that one would need to introduce other factors to explain why competition is relevant. Possible factors include order monitoring costs and information divulged in order updates that would lead to something like an effective min tick size even if the exchange does not enforce one. Competition would tend to increase monitoring and decrease the information content in orders, so that orders are updated more frequently. This would cause the effective min tick size to decrease and lead to greater pass through.

I am not ready to make a rigorous argument though.

The broker is legally obligated to purchase the security at whichever exchange offers the best asking price. The legal requirement does not incorporate taker fees charged by the exchange when computing the best asking price

OK I did not know this. This definitely does seem like the sort of distortion that would cause maker/taker fee models to be attractive.

That said, I would note that all of the reasons given so far that I find credible (minimum tick sizes, legal requirements such as what you give above) seem to be artificial ones created by traditional securities law, and crypto exchanges don’t have these limitations at least at present. So my point about maker/taker models and traditional models being equivalent still stands for crypto exchanges, except possibly for the fact that maker/taker models seem more attractive to makers and reduce apparent spreads so it’s better marketing to display things that way, much like displaying prices with tax not included.

You are assuming that having a minimum tick size or other types distortions is undesirable. This is not true when you have externalities as is the case here. In a two-sided market enforcing collusion on one side of the market generally makes both sides of the market better off. This arises because of cross-side externalities (see the paper I linked to earlier).

My interpretation of your argument would be that crypto exchanges should introduce minimum tick sizes to make liquidity rebate programs more effective. I agree with that.

I am not convinced that liquidity rebates completely wash out in the current system. You need a more complex model that accounts for a range of possible frictions to demonstrate this. Ignoring the prevalence of tiered programs, which do exist on crypto exchanges, is a major oversight.

Think about the decision to be a maker vs. a taker, the maker’s price decision, and the relationship to these decisions to the probability of immediate order execution.

Someone with valuable private information or a retail broker (e.g. Coinbase) charging a large commission will place a high value on certainty of immediate order execution.

The taker’s order executes immediately with probability 1, so If certainty is sufficiently important than you always become a taker.

As a maker, the probability of immediate execution depends on how aggressively you outbid competing offers. If the current bid-ask spread is 0.5% and you make an order that offers a spread of 0.1%, then it highly likely to get taken immediately (though not with probability 1).

The maker taker fee structure limits you to a minimum allowable spread, so that it is not possible to create a maker order that will executes immediately with very high probability.

This forces makers who require near certain execution to become takers and accept a spread of 0.0% instead of say 0.1%.

Thus, the maker-taker fees structure extracts a rent from retail brokers and informed traders and transfers it to market makers.

This won’t work if the exchange market is highly competitive because then the brokers and informed traders would simply migrate to exchanges that do not use make-take fees.

The maker-taker fee structure has nothing to do with narrowing the spread, although that effect is consequential. The spread is not caused by any single market maker, but by a collective, i.e. market maker A may quote bid-ask at 100-105 while market maker B may quote bid-ask at 98-101, thus the NBBO (national best bid offer) is 100-101. The spread is narrowed with increasing participation from any attractive fee structure.

Even then, just because the spread is very narrow does not mean the liquidity in the order book is real. For example, a market maker may be co-located near exchange servers to have first priority in receiving incoming orders from others before such orders are posted. And if the incoming orders are going to impair the market maker, it has the incentive (and ability) to change its bid-ask orders. From outside perspective, the liquidity simply disappears. “Experts” would be quick to say that’s just stale orders.

You may have all sorts of theories on the fee structure to the point of reconstructing it into a perfect structure for the most perfect market condition but you may be surprised when market inefficiencies continue to persist. The fee structure does not have 100% direct correlation to the spread.

I wonder why are we discussing about this anyway. Not useful of time and brain power.