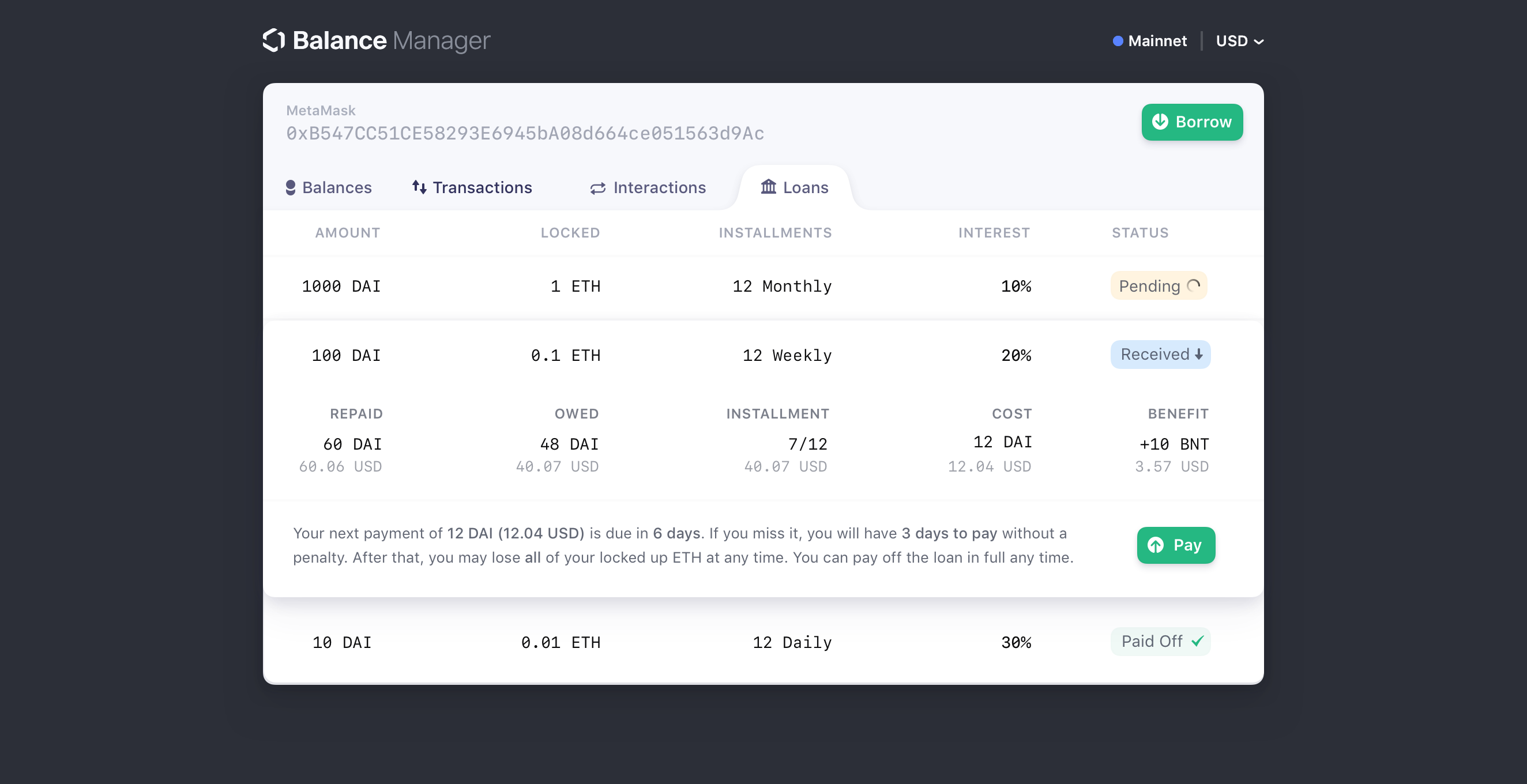

I think that fully collateralized, or more likely over-collateralized, loans are probably the only way to go at current. You see this kind of thing in traditional financial markets where people might have limitations on what they can sell (an executive selling his company’s stock, for example) so they throw a lien on their holdings to borrow cash. It’s pretty common.

Here it’s entirely reasonable to lock the collateral up in a contract and transfer it to the lender upon default. I’m quite fond of users just posting the collateral they want to offer up and leaving the onus of credit risk analysis on the lender.

Hey @SRALee one usual approach is going the “financial system” way and use traditional underwriting techniques in an on-chain fashion such as:

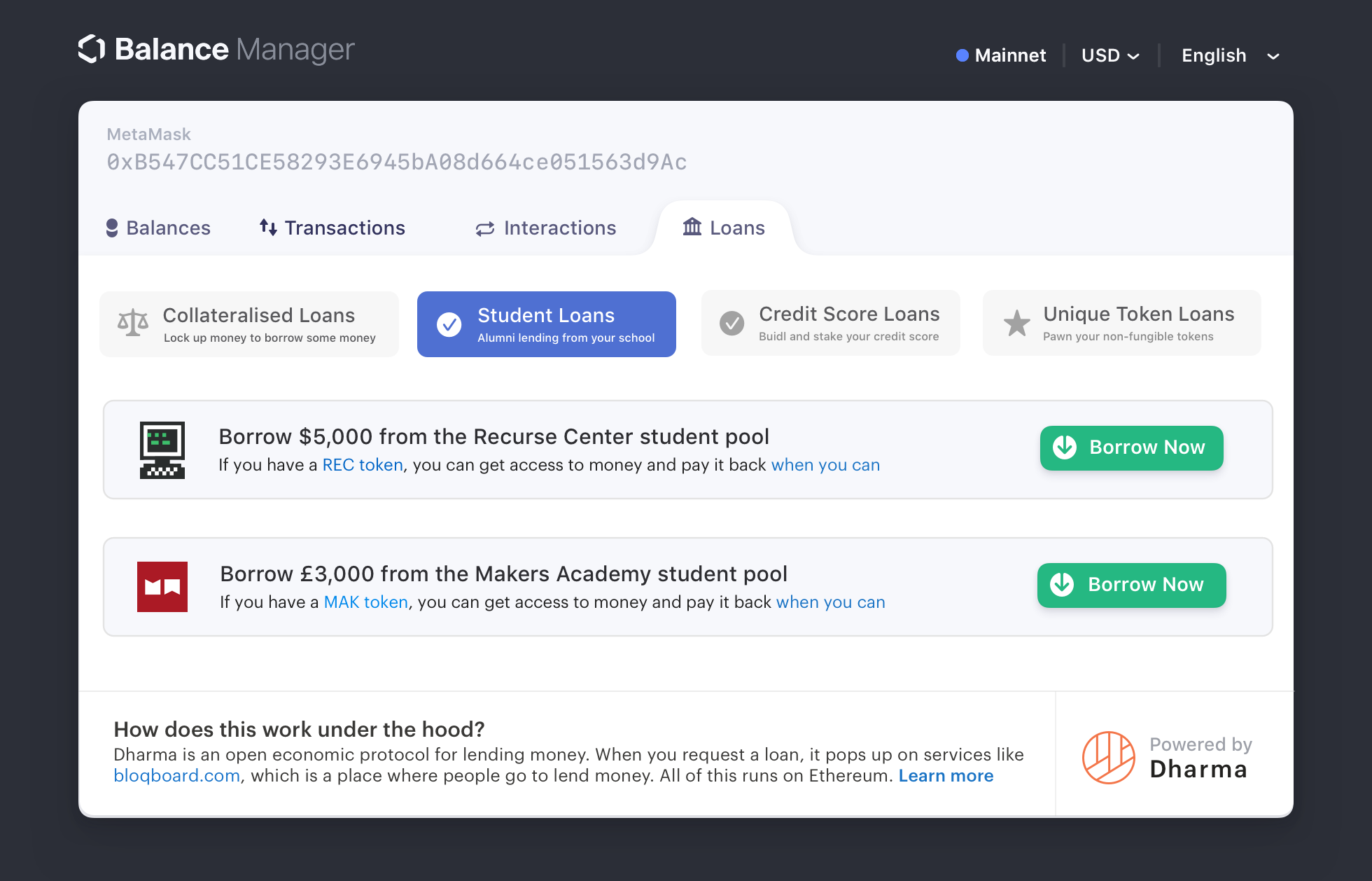

Decentralized collateralization mechanisms as used in the the “DAI stableoin System” and Dharma

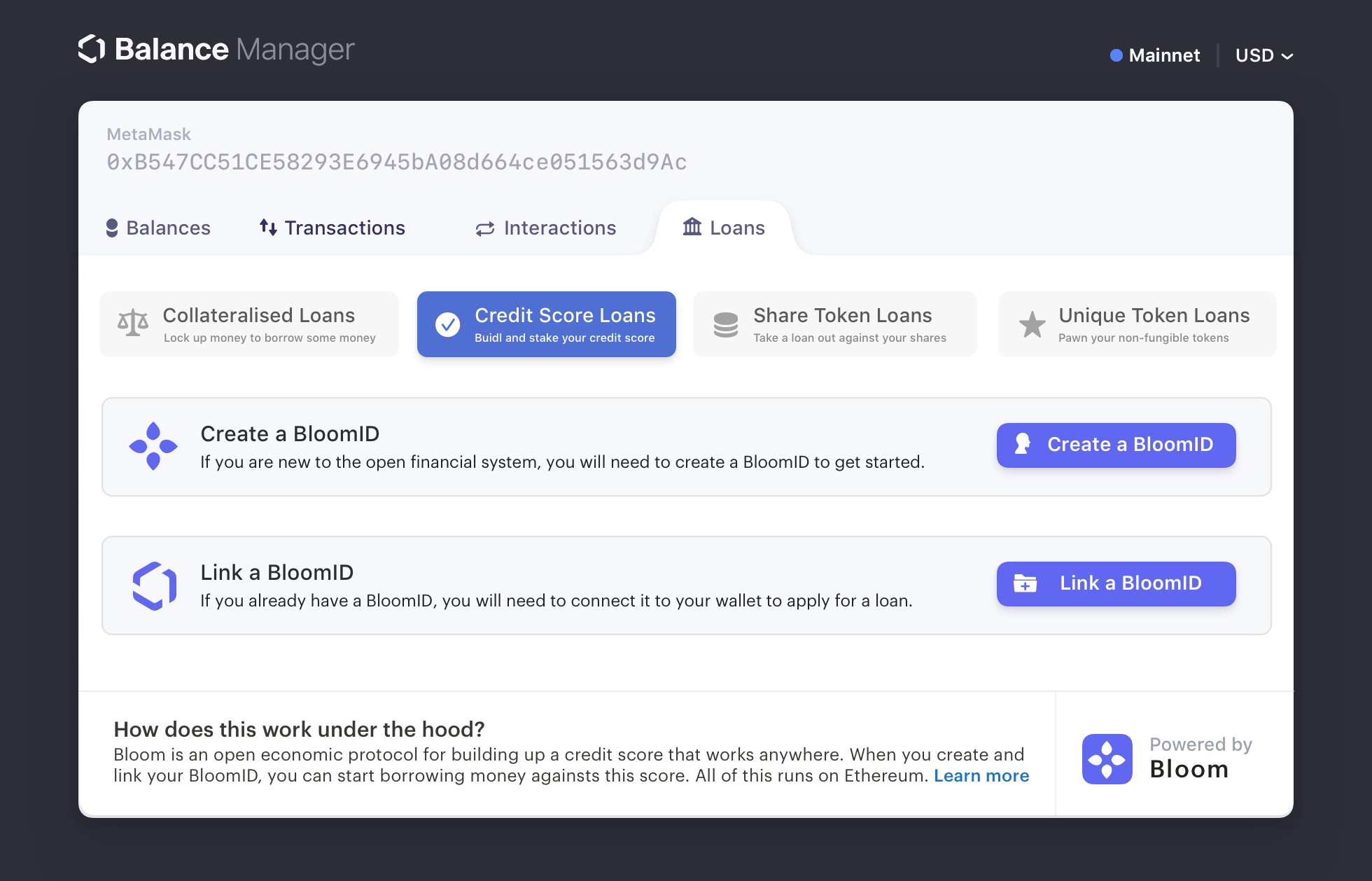

Decentralized credit score like bloom

Decentralized ID like uport

Another approach is based on off-chain reputation / identity, and informal and formal off-chain enforceability. In these approaches the end-goal might not be credit / loans itself, but rather be using these credit agreements to facilitate “money transfers without money movements”. Real-world (non-ethereum) examples of this includes:

The ancient Hawala system

Corresponding banking system

The original Ripple Idea (RipplePay) by Ryan Fugger from 2004 (Now turned Ripple.com)

Implementing a sybil resistant credit network on Ethereum

We are currently building https://trustlines.network/ which is an open-source credit framework using elements from both approaches. Basically users can enter into “trustline” credit agreements stored on the Ethereum blockchain which in a standard currency network is non-collaterized and not requiring ID/creditscore.

As mentioned this type of credit is useful to create a payment network, in which everyone can issue their own credit/money which comes with fungibility limited by the available path within the network (similar to how commercial banks issue 97 % of credit/money in circulation today).

If you are interested in learning more about the basic principles please see:

For an initial introduction to the project from EDCON last year:

Please go through the previous ETH lend and SALT ICO whitepaper (over collateralized loans) and bitbonds ( non collateralized - based on amazon credits profile, ID strength accross facebook, linkedin networks ) and let me know your thoughts ( especially SALT as I believe it uses an onchain only smart contract oracle to handle defaults)…

I wouldn’t want to re-invent the wheel if a solution aready exists ;)!

A thought experiment on using state channels for debt:

I’m imagining a state channel hub connecting borrowers and lenders for a subset of microloans.

A borrower and lender commit funds to access a lending channel hub. Those funds are locked up and, in exchange, the borrower and lender receive non-fungible tokens. Theses NFTs represent access granted to the channel hub and also tie borrowers and lenders to their respective transaction histories. For the borrower, the NFT and the committed funds behind it also represent collateral against the loans.

If a borrower defaults on a loan, the lender can seize the collateral behind the borrower’s NFT

If a borrower defaults on a loan, the borrower loses the NFT and as a result:

Loses the funds behind the NFT

Loses the access to the lending channel hub that the NFT grants

Loses the borrowing history built up over time attached to the NFT

Here, the lender’s risk is mitigated by the collateral, but the borrower has even further financial and reputational incentives to not default.

I’m not an expert on state channels and may be making incorrect assumptions here.

We have been evaluating this space for a while now but specifically the use-case of unsecured micro loans. That aside I think our research may be of use to you in regards to what is required to deliver that service.

We found that before one can even offer credit or loans (or any service) we need a secure and reliable way to record, verify and share data, eventually building up a “Web of Trust”

We have recently released a paper that demonstrates how this can be achieved.