Not to my knowledge, though I wouldn’t be surprised if some network somewhere had an isomorphic construction, or already discussed these (I put some of my own references/inspiration in the links). I was referred to Celestia light nodes as possibly relevant, to my knowledge they are not incentivised, but the links between these (and many other constructions of “light clients” in various shapes and forms) and light services deserves to be explored further. I can think of many ways that the consensus/protocol will require more services in the future, e.g., obtaining proofs/sampling, and maybe there is a more general principle at play.

It’s a fair question, I am not sure ![]() The starting point of this post was “two-tiered” staking mechanisms as described by e.g., Dankrad or Vitalik (links in post), but I couldn’t square the dynamics of the two tiers without introducing the “four quadrants” separating between the heavy/light and operator/delegator mixtures. So I was calling all this “two-by-two-tiered staking” at first, which is not very catchy…

The starting point of this post was “two-tiered” staking mechanisms as described by e.g., Dankrad or Vitalik (links in post), but I couldn’t square the dynamics of the two tiers without introducing the “four quadrants” separating between the heavy/light and operator/delegator mixtures. So I was calling all this “two-by-two-tiered staking” at first, which is not very catchy…

Anyways, it seems like these ideas of enshrining some separation between operator and delegator come back in the discourse frequently enough that we might be ok with some level of complexity. We could call a basic operator/delegator separation Level 1: Adding the gadgets discussed in the heavy layer section and otherwise business as usual, validators are responsible for Gasper, inclusion lists etc.

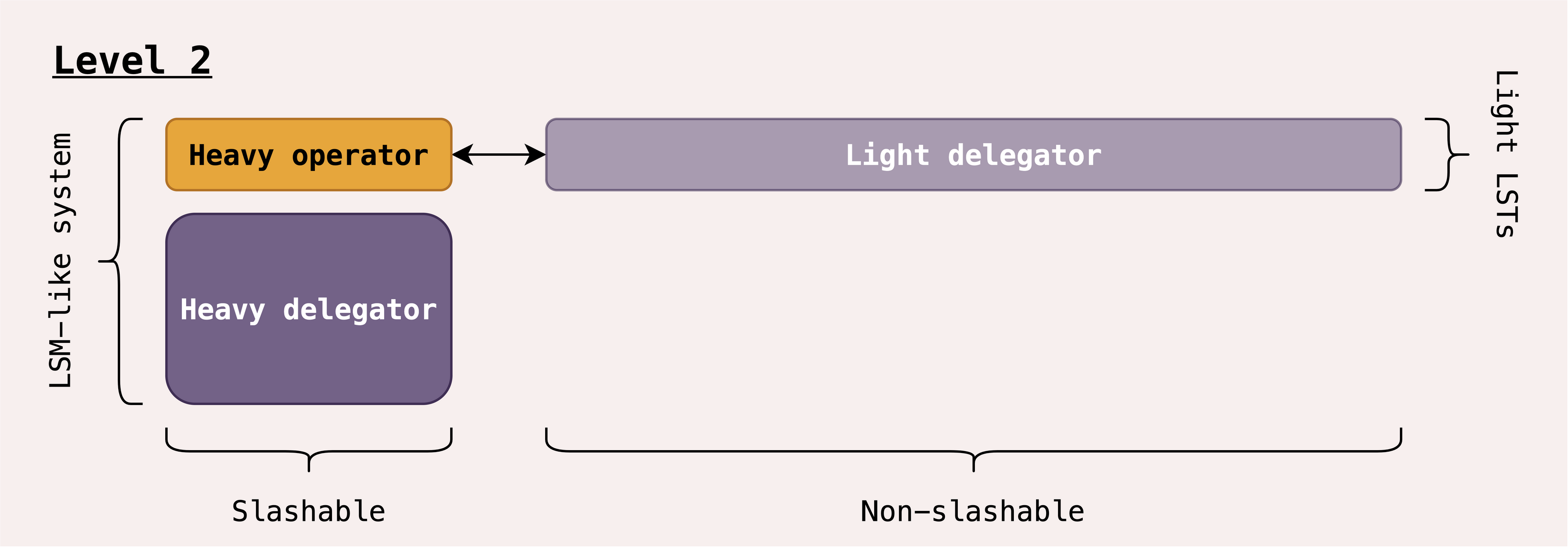

If we wanted to go further, we could go to Level 2: Create a class of light delegators which is bound to the heavy layer operators. This is closer to the two-tiered staking proposals, but recognising that the slashable tier will itself be unbundled between operators and (heavy) delegates, something that Mike was also getting at in his Goldilocks piece. The light delegators can choose to attach their light stake to their favourite heavy operators, and you then attach the responsibility of performing the light services to the heavy operators they choose. I would picture it in the following way:

And then Level 3, which is the full rainbow staking model with enshrined light operators, as discussed in this section.

I think we should move away from a monolithic view of “solo stakers”, even today it is quite a diverse set between those that stake with their own capital and hardware and those that are part of LSPs (where here I mean solo staker == permissionless operator), and then there is also the question of who participates in re-staking etc. So it would be hard to quantify with just one number that we try to maximise. Perhaps a better benchmark is the revenue captured by the set of permissionless operators, as a fraction of the total operator revenue. We might have the “right” number of permissionless operators today, but what’s less clear is their economic sustainability over time. By creating a source of revenue for which we have strong(er) reasons to believe it will sustainably benefit this set of participants, we can target the correct amount more easily.