Validator Redirected Revenue

I. Executive Summary

-

Ethereum is stuck in a coordination failure: everyone benefits from shared improvements but no single actor wants to pay when others can free-ride. This creates a persistent deadweight loss that weakens Ethereum’s long-term competitiveness.

-

The proposal introduces 2 changes at the protocol-level to create a funding mechanism driven by validators, who configure

-

% of staking rewards redirected to ecosystem funding: If a majority of validators agree to part with a share of their staking revenue, the redirect rate becomes mandatory for all validators.

The maximum amount in redirects is 10% of staking rewards, beyond which no increase would be possible, while the minimum is 0% (current status quo). At a protocol level, the parameter change is (UP/DOWN/ABSTAIN) where UP or DOWN increase or decrease the redirect amount by fixed rate e.

-

Preferred funding recipients: Validators also indicate their preferences for the recipient address where they want the funds to be redirected. Execution clients take in these static preferences to come to a consensus on a splitter contract dividing funds between the different addresses, based on the split that would win in a head to head duel against all other possible splits (a solution concept called a condorcet winner).

At a protocol level, the parameter change is (KEEP/CHANGE/ABSTAIN) where KEEP maintains the existing splitter contract while CHANGE results in a new splitter dividing the redirects between the funding recipients indicated by validators.

-

The key advantages of the design are minimized governance overhead for validators who simply “set and forget” their inputted preferences on redirect amount & recipient addresses, with execution clients figuring the rest out (we expect healthy diversity in their implementations). Another advantage is simplicity at the Protocol level, which only cares about Increase or Decrease for the redirect amount and Keep or Change for the splitter contract determining where redirected funds go. The primary concern is principal-agent issues between staking operators setting the configurations and those delegating their ETH to them.

The goal of the post is not agreement on the proposed solution so much as discussion around the need to address underfunding at the protocol level and a “wrong answer” to spur debate. Accordingly, the next section focuses on the main issue in need of redressal (reducing deadweight loss in the Ethereum economy) before moving on to why validators have the incentive alignment to become a long term stakeholder that addresses it. The fourth and fifth sections respectively touch on the proposed solution and the open challenges they introduce.

II. Free Rider Problem and Deadweight Loss in the Ethereum Economy

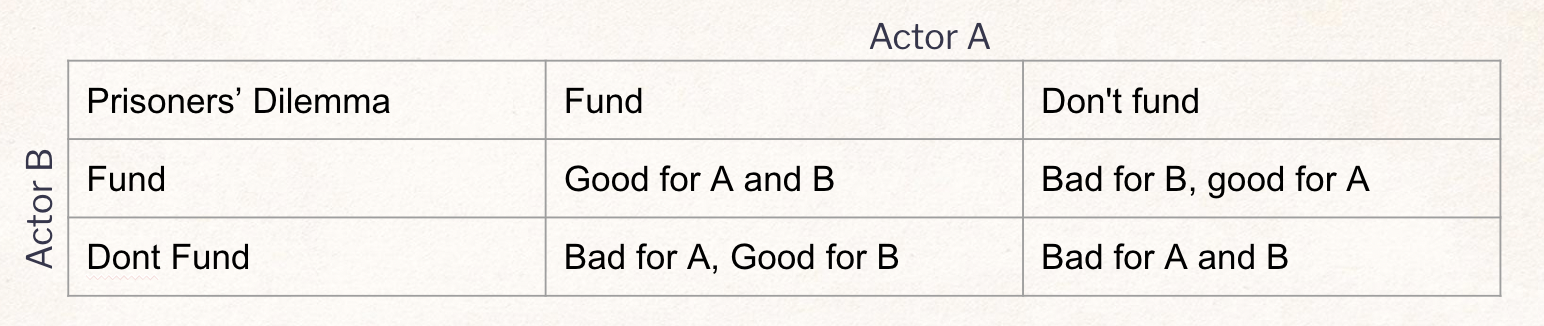

The funding challenge in Ethereum resembles a classic prisoner’s dilemma.

Consider two actors who both care about Ethereum:

-

If neither contribute, both retain their capital.

-

If one contributes and the other does not, the contributor sacrifices while everyone else benefits at his expense

-

If both contribute, the ecosystem grows and both benefit

While the third outcome is collectively optimal, each individual faces an incentive to defect from the funding coalition and free ride on the contributions of others.

This dynamic leads to Ethereum getting stuck in a stable but inefficient equilibrium where no one contributes, even though everyone would benefit from coordinated funding.

The same problem appears in many economic systems. Voluntary payment for public goods rarely succeeds because individuals hesitate to contribute when others can benefit without paying.

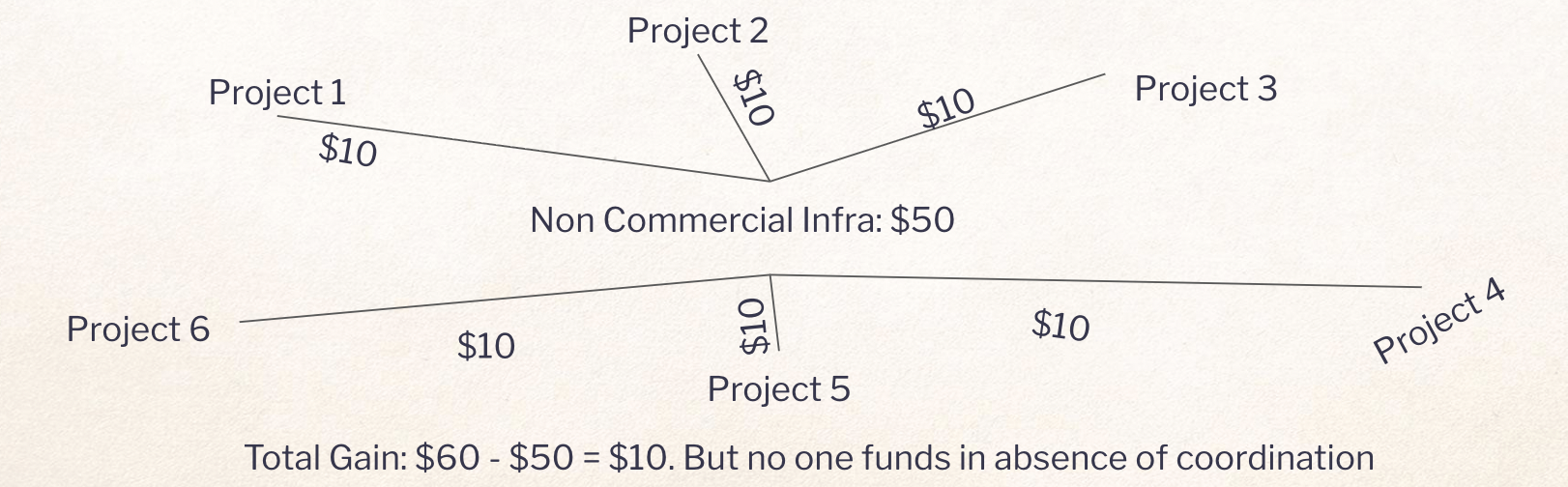

This creates a deadweight loss in the Ethereum economy, a concept that can be explained with the following example;

-

A piece of shared infrastructure costs $50 per year to maintain.

-

Six projects depend on it.

-

Each project gains $10 in value from the infrastructure.

The total value created is $60, which exceeds the cost of $50. From the perspective of the ecosystem as a whole, the project should clearly be funded.

Economists refer to the $10 as deadweight loss, an irrecoverable cost making economies uncompetitive

However, no single project receives enough value individually to justify paying the entire $50. As a result, either

-

The infrastructure never gets funded, although it would benefit everyone collectively

-

The Ethereum Foundation funds the infra to reduce deadweight loss, either directly or by bearing the coordination cost of getting all relevant projects to cough up the $10

-

Some philanthropist steps in to cover the entire cost

Economies that reduce deadweight loss tend to outperform those that cannot. Successfully coordinating shared investment is essential to compete with both traditional economic systems that use coercive measures like taxation to reduce their deadweight loss and corporations that reinvest earnings back into future growth.

III. Validators Benefit from Ethereum Growth

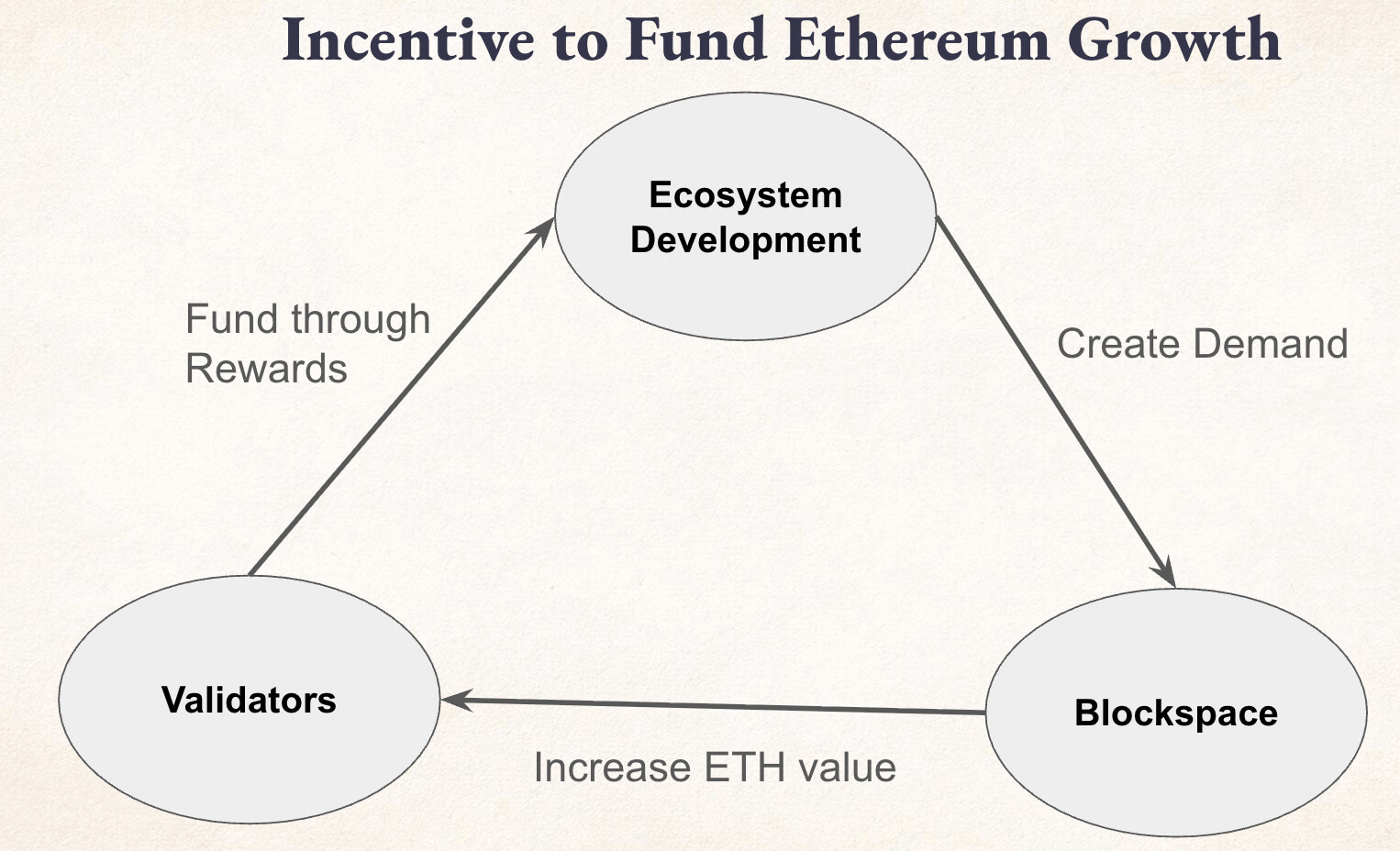

At a structural level, validators have a clear incentive to support Ethereum’s growth.

When more applications, tools, and infrastructure are built on Ethereum, demand for blockspace increases. Greater demand for block space strengthens the network’s economic activity and overall network value.

Since validators stake ETH and earn rewards denominated in ETH, they directly benefit from the long-term growth of the ecosystem via the following positive feedback loop:

-

Validators fund ecosystem development.

-

Ecosystem development increases network demand.

-

Increased demand leads to more ETH burn.

-

Validators benefit from higher value rewards and increase in value of principal staked

Despite this alignment, why don’t we see much funding coordination by validators outside of promising but isolated efforts such as the DAO Security Fund or Octant?

Our hypothesis is that it is due to validators getting stuck at the non-cooperative equilibrium in the prisoners dilemma, where they would greatly benefit from funding the ecosystem with their rewards at a non-zero amount, but the reality of defections by other validators makes most of them hesitant to contribute anything. Accordingly, we present a solution in the next section to address the free-riding problem.

IV. Validator Redirects: A Protocol-Level Coordination Mechanism

The core idea is a protocol level change where validators need to signal 3 things;

-

Ability to handle an increased gas limit (already exists)

-

% of staking rewards redirected towards the ecosystem (requires hard fork)

-

The recipient address that should receive these redirects (requires hard fork)

We will now separately tackle each of the 2 proposed changes;

- Redirect Rate

The key element in (2) is a majority-trigger mechanism: If 51% of validators signal a redirect rate above 0, the contribution becomes mandatory for all validators. At that point, every validator contributes the specified portion and sees their rewards fall by the corresponding amount.

This approach addresses the free-rider problem. Validators can commit to funding without risking unilateral disadvantage, because the contribution only activates once a majority agrees.

In effect, the protocol would enable validators to move from a prisoner’s dilemma equilibrium toward cooperation. The Nash equilibrium we expect validators to converge on is,

Loss of staking revenue = E[Extra Value to ETH]

There is some free-riding still present as ETH price increases benefit everyone and not just stakers. So the mechanism would still underfund compared to the optimum as stakers would increase the share of funding up to the point where

Loss of staking revenue = E [gains from eth price appreciation for stakers only]

Where does the extra value E come from? Apart from the efficiency gains of reducing deadweight loss by collective investment, by helping us break out of the following loop

a) People are scared Ethereum is gonna lack funding in the future.

b) They decrease their estimates of Ethereum’s success.

c) They decrease their valuation of ETH.

d) ETH price decreases.

This design only partially addresses the free-rider problem, as ETH holders who are not staking would still benefit from redirects made by the validators. But within the set of all validators, redirects are optional for the group but mandatory for the individual. This is an improvement over the traditional economy’s solution to the problem of deadweight loss reduction (taxation) where there is no opt-out.

We propose capping the redirect rate to a maximum of 10%, as a natural schelling point given the history of tithe and norms around contributing 10% of earnings back to society. Moreover, the cap limits the theoretical worst case scenario of redirect dialled up to 100% for redistribution to a bad actor, which the next section tackles more comprehensively

At current levels of ~35-40 million staked ETH and 1.91% rewards, approximately 700k ETH per year is currently given to validators for keeping the chain secure. A redirection of even 5-10% provides significant funding to the ecosystem (approximately 50-70k ETH per year) without exerting undue force, since validators preserve the option of putting the redirect rate all the way down to 0% (status quo).

- Redirect Recipients

While determining the redirect rate is relatively straightforward, a more complicated question is figuring out how the funds should be allocated.

We’ll divide this section into 3 questions; how validators indicate preferences, how they get aggregated, and final construction of the list of redirected recipients.

Q1: What changes do validators need to make under this proposal?

At a validator level, all that is required of them is specifying

-

the contract addresses or EOAs that should receive the redirected funds

-

the % amount to each.

For example, a validator may put 0xABC… as 60% and 0xXYZ… as 40%. Unlike other mechanisms that require frequent participation, the validator can simply set and forget, with the option of manually changing their preferences at any time (in practice, we expect defaults to become sticky once set). This approach ensures that validators, the ones who are parting with revenue they would have otherwise earned, retain control over how their money is distributed.

We can now move to the next question,

Q2: How do we aggregate heterogeneous validator preferences into a single splitter contract that defines how funds are distributed?

Upon execution of the proposal, the mechanism starts with a 0 redirect rate and a 0 address as redirect recipient. Every 128 blocks (approximately 5 minutes), the first validator can propose a new candidate splitter contract to become the new ‘King of the Hill’ by knocking out the existing one. If the candidate better aligns with the configured preferences of validators, it becomes the new King of the Hill splitter contract. If it is equal or lower in alignment to the validators preferred recipients, then the existing King of the Hill is maintained.

We have now reduced the problem in a way to tackle the final question on final list,

Q3: How do we gauge whether a candidate splitter contract better aligns with validator preferences than the current King of the Hill?

We propose that the mechanism use a distance metric (such as Manhattan distance) to determine whether the protocol should KEEP or REPLACE the existing king of the hill. As an example taking 3 redirect recipients;

Validator ideal distribution: [20%; 0%; 80%]

Existing King of the Hill splitter contract: [50%; 25%; 25%]. Distance of 30%+25%+55%= 110%

Candidate splitter: [30%; 50%; 20%]. Distance of 10%+50%+60%= 120%

So the validator automatically votes to keep the current king of the hill as it is closer to preferences compared to the proposed alternative.

There would be some degree of diversity in how execution clients implement methods of comparison between candidate and king of the hill splitters, such as convex utility functions (eg: either attribute a large amount to a mechanism, or none at all, but not something in the middle). Validators may also adjust the amount allocated to the splitter contract all the way down to zero if they are unhappy with how funds are being allocated. Overall, this “king of the hill” mechanism will converge to a distribution of funds that is a condorcet winner: a distribution that would beat out any other distribution in a head-to-head vote. It also ensures simplicity at the protocol level where the options are only to “KEEP” or REPLACE” the existing splitter contract.

V. Open Issues

While the proposal helps address coordination problems around funding, it raises some intractable concerns that must be addressed.

1. Validator Cartelization

The most significant risk is cartel formation.

If a majority of validators collude, they could theoretically crank up the redirect rate and redirect those funds back to themselves. For example, 51% of validators could vote to set redirect rate to the maximum 10% and set the redirect recipient to a splitter dividing the money between them, thus ‘stealing’ staking rewards from the other 49%. There is an element where the drop in price from collusion makes such malicious actions economically unprofitable.

2. Principal-Agent Problems

The problem raised in (1) becomes more acute when we take staking operators into account.

Currently, roughly 90% of ETH is staked through operators rather than solo stakers, who become validators using the capital provided by customers. Operators are typically incentivized by a percentage of staking rewards, whereas ETH holders care primarily about the long-term value of their principal.

If operators control the preference setting mechanism, they may prioritize redirects to projects that benefit them, such as an improved operator experience, which their users care little for. The best answer to this issue is a competitive market of staking operators that customers can migrate to if they don’t like their voting preferences for redirects.

3. Issuance Signaling

Another implication is that validators signaling willingness to contribute part of their rewards could be interpreted as evidence that Ethereum’s issuance rate is higher than necessary.

Validators’ willingness to give up 10% of their rewards could be interpreted as an ability to reduce issuance by 10%.

Rejoinder

Today, most users select operators based on purely financial value (yield and risk).

If such a mechanism were implemented, a new dimension of competition gets added where users choose operators based on values. For example, a user may prefer staking with an operator that sets redirect rate to 5% and recipient to a team making Ethereum quantum resistant. Some operators may also let users directly set their preferences.

Over time, this could reverse centralization of staking operators as values are inherently more pluralistic than the network benefits to scale that financial returns enjoy. It may also encourage more solo staking, since individuals would have direct influence over how important projects in the ecosystem get funded.

Moreover, under the voting mechanism we’re proposing, cartel behavior isn’t stable. That is to say, if we assume that validators are purely driven by greed and seek to use this process to funnel more money to themselves, the “king of the hill” option will never settle to a stable distribution that gives any validator more than they would get under the current status quo. See the appendix for a mathematical explanation.

The issuance reduction debate is broadly in 2 camps; one side believes that any cuts should only be made after lean ethereum to preserve reliability, given that institutions have built their staking products with certain assumptions in mind. The other side believes the issuance curve is flawed as it does not taper with more ETH staked, and an adjustment is required as early as Q1 2027. This proposal works independent of the issuance debate; nonetheless, given the need for core ethereum funding, there is a happy path where redirects serve as a better alternative to pure cuts.

Next Steps

We seek further feedback before working on a technical implementation to put forth as an Ethereum Improvement Proposal. The post immediately after this will have an FAQ that will be updated as questions come in.

Even if there are irresolvable concerns preventing acceptance of the EIP, we think it essential that there be a contingency plan that can be activated in an emergency so that we do not start at 0 during a crisis.